Opportunities in the Agent Era

Over the last several months, it’s clear we’re entering a new era in technology focusing on agents.

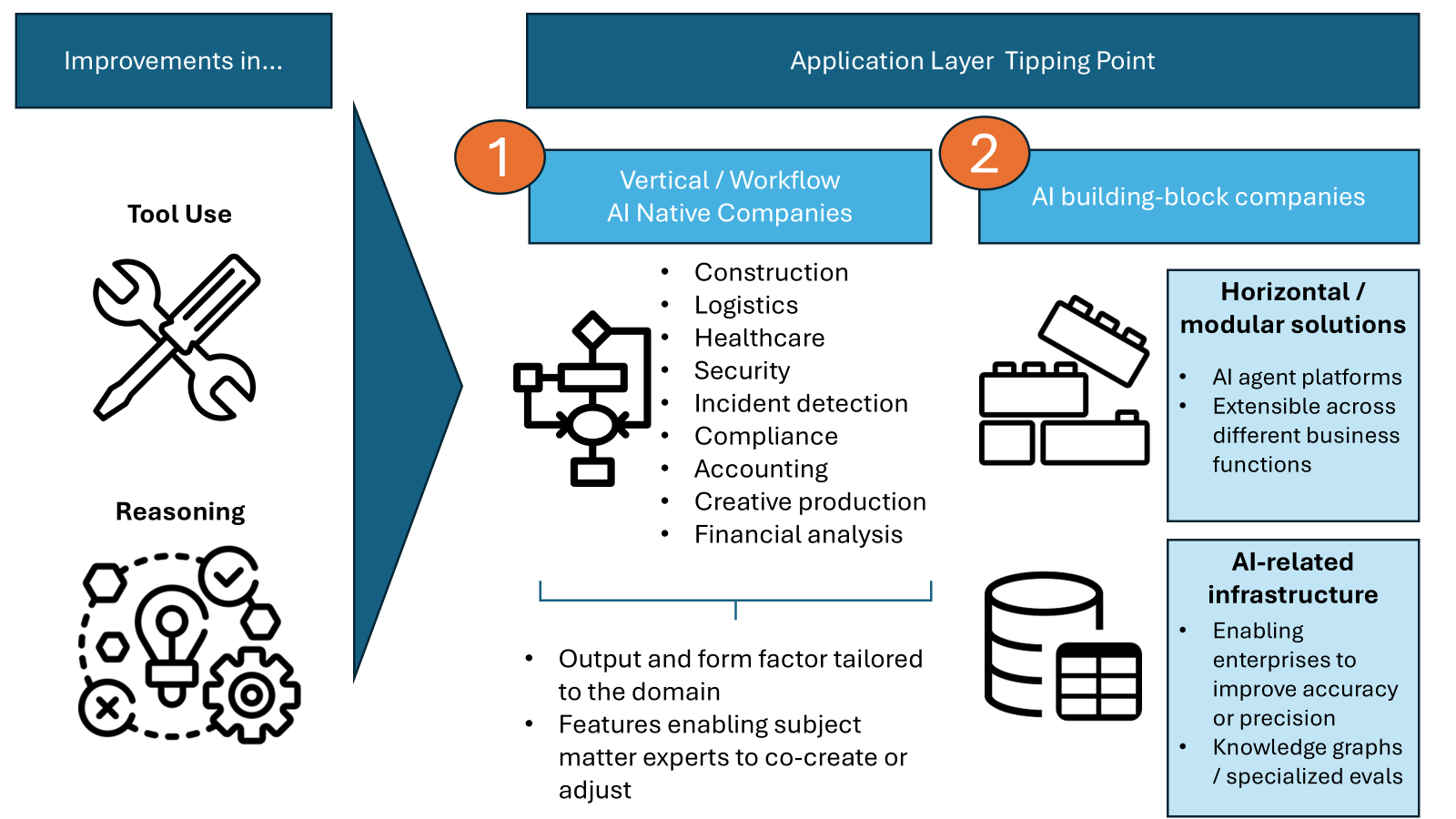

The key enablers behind this are two-fold: first, improvements in tool use and tool interactions (browsing, retrieval, memory, plugins, code interpreters) revolutionizing how AI interacts with software, and second, the emergence of more advanced reasoning models (unlocking the ability to plan and execute complex, multi-step processes) allowing AI agents to solve problems that once required human intervention.

This will result in an explosion of use cases, because now we have the capabilities to build systems that can reason and act on data - both structured and unstructured - across multiple surfaces (i.e.: across programs, using browsers). This opens up the floodgates when it comes to opportunities for value creation.

Why this is a massive opportunity

The ability to work across fragmented systems, combining structured and unstructured data, is a huge unlock.

Think about modern workflows. You might spend six hours in meetings, send 20 external emails, have 40 chats across programs like Slack, WhatsApp, LinkedIn. Those meeting transcripts, emails, instant messages - unstructured data previously not accessible to previous generations of software - have invaluable insights about customer goals, challenges, competitor insights.

Until recently, extracting and leveraging those insights at scale was nearly impossible. Now AI can extract insights from this data, to transform core business functions:

Marketing: imagine automatically identifying which product features captivate customers on demos, so you can build a campaign on those specific features

Sales: picture the ability to create a running list of sales objections weekly, giving the ability to provide tailored coaching across the organization, to help win more deals

Customer service: envision creating a report flagging customers who are beginning to show signs of frustration, enabling proactive outreach before issues escalate.

Product Development: imagine holding user interview sessions, and being able to create a feature prototype demo in that same meeting, accelerating feedback cycles and time to market

Augmentation to Automation Spectrum

In this agentic future we’re entering, where agents can do all the work, a key question becomes to what extent should they be doing all the work? Where to land on the automation spectrum? For teams embarking on an AI integration, the journey from augmentation to automation involves several critical questions:

Which customer segment should you serve?

How sensitive is the service and the customer segment to errors?

What efficiency gains can you achieve today if you automate with AI? What about tomorrow, as the models get better?

What are the compliance and security requirements for the industry that you’re seeking to solve for?

We’ve seen some ways this has played out, in verticals with early AI traction, such as coding or customer service.

In the code generation space, serving obviously technical customers (engineers), the trend has been to move in the direction of automation. Initially the dominant approach was co-pilots (GitHub Copilot), then integrated developer environment’s (AnySphere’s Cursor, Codeium’s Windsurf), and now products offering autonomously running agent offerings (Factory AI, Reflection AI).

In the customer service space, where key stakeholders are non-technical business line owners, and where use cases involving full automation pose greater risks (reputational, security-related when combining public access points with payment data or customer information), the approach has been more measured. While some companies like 11x have made automation a core component of the offering (and this for lower-risk customer-facing activities like outbound SDR products), other companies have taken the opposite tack, focusing on the augmentation approach. An example here is Melody Arc, which uses AI to improve the efficiency of frontline workers, offering suggested answers and more efficient call routing, but making the human / AI interaction the key value proposition for its product.

That said, whether it’s augmentation or automation, nearly all of these agentic solutions have an impact, either in terms of labor savings or improved labor productivity.

Opportunity Areas

Which areas represent the greatest opportunity for builders? Winners will likely be concentrated in two primary categories:

AI native, workflow-focused companies: many of these will be vertically focused, along the augmentation to automation spectrum, with outputs and form factors tailored to a particular domain. Also critical in this bucket are features that enable subject-matter experts to co-create, through adjusting or error correcting

AI building block companies: companies focused on horizontal and modular solutions, including AI agent platforms extensible across different business functions and AI-related infrastructure enabling enterprises to more easily improve the accuracy and precision of their AI deployments

1. Workflow / Vertical AI-Native Companies

Teams focusing on the application layer, more than ever, need a combination of technology chops but also deep domain expertise (either builders coming from the industry, or with a forward-deployed engineering mentality).

Why is this? Because of the many challenges enterprises have today moving AI into production. First, enterprise data is fragmented, sitting in many different systems requiring huge efforts to compile. Then, AI deployments often involve multiple moving pieces – one has to map the task needs (accuracy requirements, domain specificity), with infrastructure components (choices around RAG architecture, embedding setups), and those different combinations all involve trade-offs (accuracy, latency, cost, ability to handle edge cases). Building trust, ensuring repeatability in solution deployments takes time, and involves validation from both technical and (crucially) non-technical stakeholders.

Achieving high accuracy and solving stakeholder specific needs takes time, but once a robust solution is in place, enterprises have shown in this current building cycle a willingness and ability to pay large dollar amounts for solutions that meet their needs. Hence, compared to historical startup building patterns, a team’s ability to take a forward-deployed approach (or have a founding team with deep roots in an industry) is an important differentiator. And one that can develop into ‘earned secrets’ to accelerate vertical-specific product development.

A good illustration of this is a company in the AI-customer service space, Sierra, which has a deployment approach that specifically involves dedicated agent engineers and product managers for each client that signs up. The purpose of this approach is to translate the customer’s journey into agent code, oversee integration into customer systems, and partner with business teams to review agentic responses and continuously improve.

The key moat then isn’t the product itself, but the workflow. And by solving the workflow the product itself can improve as well. So, in the case of Sierra, one of the key learnings from early deployments was the need for observability solutions that were visible not just to technical users monitoring evals in machine learning platforms, but business stakeholders who wanted the ability to monitor responses and also see insights into customer sentiment. Those features were then added to their product, enabling faster validation, and accelerating trust, which shortens time to value for future prospects.

Next frontiers for building

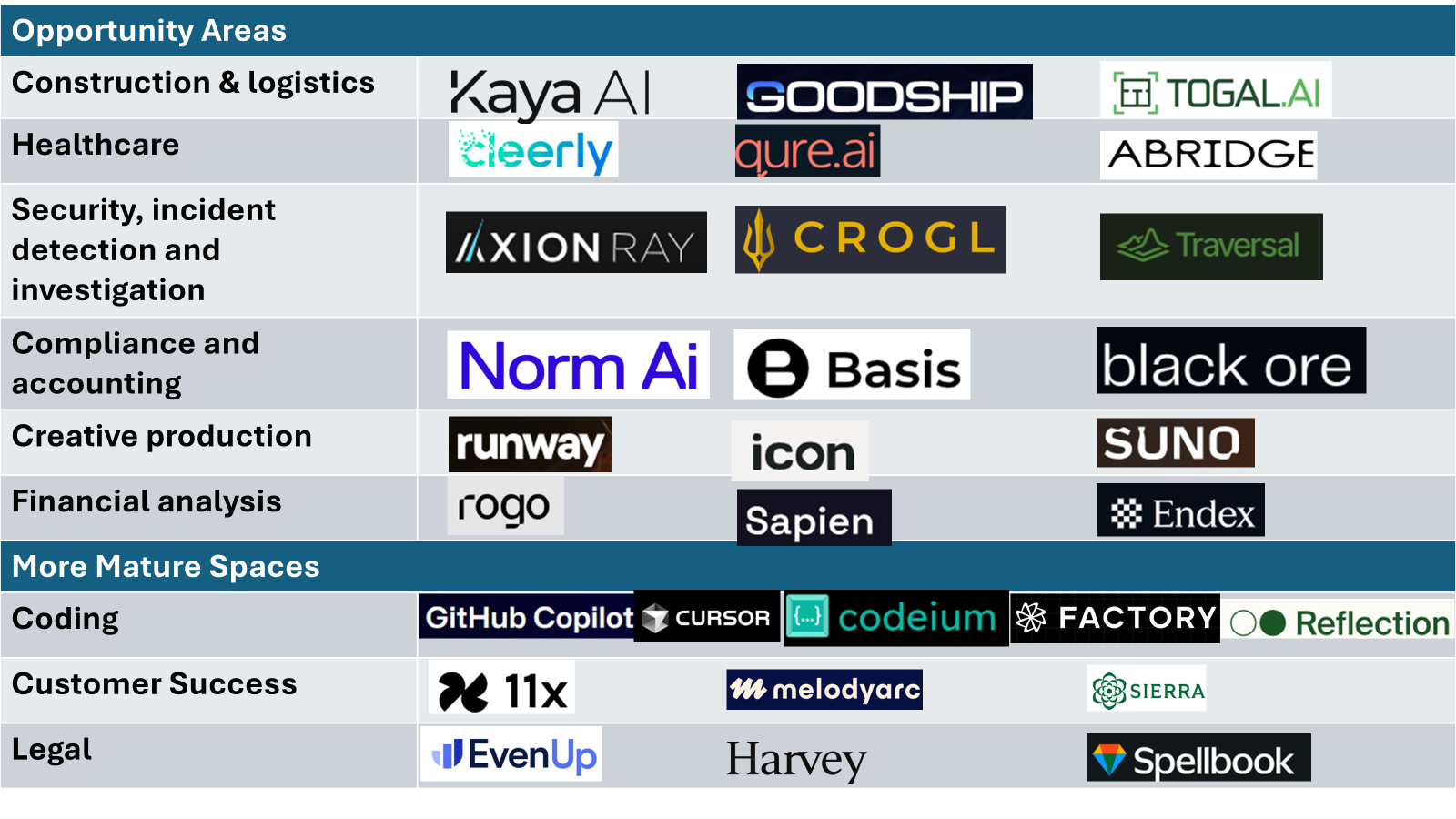

While coding, legal-tech and customer service are some verticals where multiple builders have emerged at the application layer, a large number of opportunities outside of those spaces still remain.

For high value professionals, automation solutions in the area of back office operations, procurement, billing, transcript services can be valuable by directly driving productivity (enabling these professionals to spend more time with clients and engage in higher value activities). That’s partly how Abridge, a transcription solution that frees up an average of two to three hours a day for clinicians, has become a fast growing disruptor in the healthcare industry, and was one of the reasons why EvenUp was so successful in the personal injury space (driven by its ability to automate demand letters, which directly tie to a billing event for personal injury firms, the primary customer type that EvenUp serves).

Areas to Watch:

Construction & Freight Orchestration: Platforms like Kaya, Goodship and Togal are already reimagining construction site operations, physical goods logistics, and on site visits. Kaya addresses an overlooked segment, the ~$2T construction industry, helping companies who still rely on fax and phone calls to manage delivery schedules, procurement, etc. and automate all the back office parts of the business, while Goodship, in a similar vein, is using AI to become the operating system for the ~$1T freight and logistics industry. A different class of startups, exemplified by players like Togal, are meanwhile using cutting edge modalities such as vision to address use-cases like on-site visits, making it easier for architects and craftsmen to measure spaces and shorten the time from blueprint to final design.

Healthcare: outside of a host of transcription startups, companies are using AI for areas like diagnosis and early detection. Cleerly for example is transforming how clinicians treat heart disease, using AI-based cardiac imaging to detect cardiovascular disease (the #1 cause of death globally, costing over $422B annually) faster and more accurately, while Qure is utilizing its advanced AI-imaging technology to help diagnose diseases like Tuberculosis and Lung Cancer, serving underserved populations now to 90+ countries worldwide.

Security, Incident Detection and Investigation: emerging startups are tackling important but difficult to staff areas within organizations, such as issue detection and prioritization (Axion Ray), security incident investigations (Croql), and site reliability engineering (Traversal). These types of applications are areas where AI has a major advantage, as LLMs are particularly good at anomaly detections, and with advances in reasoning, can now be reliable enough to be able to troubleshoot, identify root causes / generate reports, and more importantly, adapt and learn.

Compliance and accounting: the rule-based and classification / summarization nature of compliance and accounting are huge vertical AI opportunities. Norm AI was an early mover in the compliance category, and today the company has developed a solution that automates compliance and legal in a platform, with a robust set of checks to satisfy leading enterprise customers. In accounting, companies like Basis and BlackOre are working to disrupt the space as well. This is a space where solution providers are still relatively early stage, creating opportunity for builders.

Creative production: as multi-modal models have become widespread and cheaper, companies have tackled creative production. Runway has transformed creative production at the high end. Meanwhile a second wave of companies have emerged, such as Icon which has democratized ad creation for ecommerce use-cases, and Suno which is doing the same thing but for AI-driven music creation.

Financial analysis: improvements in reasoning could particularly turbocharge and accelerate the area of financial research and analysis. A new breed of companies have started to emerge, like Rogo, which serves more than 5,000 bankers and saves analysts on average 10+ hours per week, and Sapien which can routinize complex, multi-source report generation for FP&A teams. Meanwhile companies like Endex are using newer transfer learning approaches like reinforcement fine-tuning to create specialized, domain-specific models that are able to match expert-level quality levels, which could be transformative.

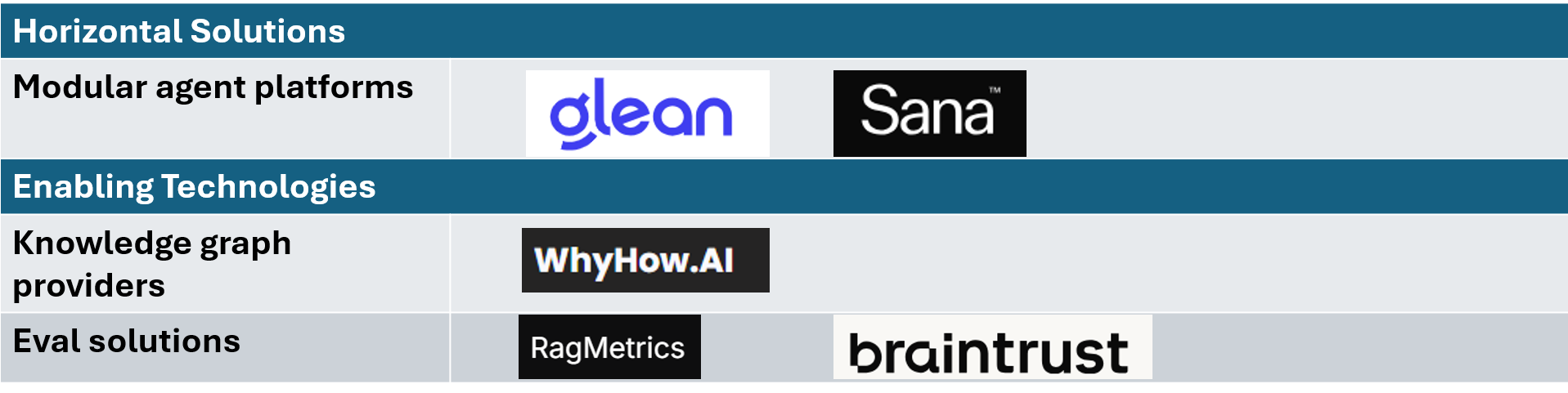

2. AI Building Block Companies

The other area to pay attention to are the “AI Building Block” companies. Those include companies that are focused on horizontal and modular solutions, and underlying infrastructure technology players that enable enterprises to improve accuracy and precision of AI solutions. Taking them in turn:

Security-First Horizontal Solutions

Modular agentic companies reflect the growing demand for low-code / no-code platforms for building AI agents in enterprises. Businesses are seeking customizable agents that can integrate seamlessly with their unique workflows, and can be assembled by people without deep AI expertise. While the accuracy or quality of solutions is dependent on the specifics of the task, setup and use-case, the flexibility these solutions provide is one of the key value propositions.

Early examples like Glean have evolved from enterprise search to power more than 50 million agent actions across its customer base, with features designed for individuals in an enterprise and templates for department or organization-wide processes. Another company in this space is Sana which rolled out its own agent development platform for use by individuals, teams and departments across the enterprise.

A key feature in both of these companies approaches is a focus on security, governance early on in their product’s rollout (a key requirement for many corporate CIOs). This essentially gave these companies a beachhead to connect to various structured and unstructured data systems across the enterprise, which later enables the development of more advanced agentic offerings that can tap into the same systems.

Enabling Technologies

While model providers will continue to release improvements to tool-calling and agentic features like OpenAI’s recent Response API launch, there is robust demand for products that can enable enterprises to improve overall relevance or accuracy of their data, as Voyager’s $220m sale to MongoDB recently illustrated (Voyager’s focus was vertical specific embeddings, designed to increase the retrieval accuracy of specific RAG applications, which could be applied to systems using multiple LLM providers).

Areas in this space that indicate promise include:

Knowledge graph providers: companies such as WhyHow that are enabling players in specific domains like legal to drive transformative improvements in terms of accuracy, which enable business-critical use-cases.

Eval solution providers: which are major blockers for enterprise adoption, with certain providers specializing in develop domain and subject-matter expert evals. Companies such as Ragmetrics and Braintrust are starting to show promise in this area.

The key principle for builders in this space is to avoid areas where the large labs are developing and likely to release features (making individual startup investments in these areas obsolete or worthless). Over-engineering architectures (using rigid prompt logic) to drive improvements in agent-decision-making would be one area to avoid given the large labs investments in agentic capabilities and improvements.

But as MongoDB’s acquisition of Voyager showed, there is still high demand for solutions that make enterprise deployments easier, and enterprise data more actionable.

Key Risks and Open Questions For Builders Today

Domain-specific model customization arrives sooner than expected, making forward deployed approaches a poor investment

As transfer learning techniques like reinforcement fine-tuning become more accessible, enterprises will be able to create domain-specific or expert models more readily on their own, removing the necessity for AI-Native Workflow companies to use the “forward-deployed” / integration-heavy approach.

Reinforcement fine-tuning is a relatively new model customization technique that allows builders to create expert models tailored to a particular domain. Previous approaches relied on complex prompting, chained completion, multiple verification steps, or very expensive custom-trained models. The impact of this technique was highlighted by the launch of Endex, which showed how domain experts graded response quality and improved the quality of responses between 6-10x, driving expert-judged win-rates from 6-12% to 70%.

This could dramatically increase the rollout of domain-specific applications (for areas like finance, healthcare) and make enterprise adoption and rollout significantly easier. We might be seeing the effect of this already, with companies like OpenEvidence targeting doctors, and companies like Bolt.New targeting programmers able to drive product-led-growth adoption playbooks.

The result could be the creation of a third category, between the modular/horizontal approach, and the integration-heavy vertical approach. If this trend continues, teams could be advised to avoid over-indexing on integration-heavy business models.

Computer Using Agent Developments Provides Tailwinds to Emerging Players, Horizontal AI Products

OpenAI’s Operator Tool and Anthropic’s Computer Use Mode make it easier to build with modular / horizontal applications, as these tools can be used to pull data more flexibly across a wide variety of applications, and the modular providers won’t be as limited by needing to build out cumbersome integrations with each data provider.

The use of these features still does not have widespread adoption among builders (due to the slow rollout, high cost of the initial releases, and accuracy concerns). But the technology is certainly one with a lot of potential, so this author is bullish on improvements in computer use making overall integrations easier (and disproportionately accelerating horizontal / modular players)

Investing in technology that the model providers themselves later provide

This happened to some builders in the Robotic Process Automation space, who did a lot of custom work that was later replaced with the rollout of the Operator Tool by OpenAI and Computer Use Tool by Anthropic. The obvious analogue in the upcoming year are startups, building agentic features that are later released by the large labs who have heralded 2025 the Year of Agents.

Even with better primitives that are released, the direction in the ecosystem is towards a convergence of performance and feature releases by the large model providers. Builders who focus on interoperability between underlying model technology, and avoid obvious areas where the large model providers are likely to build features near term are best positioned, but there is no doubt that the space is hard to predict in greater than 6 to 12 month increments

Underestimating Change Management Challenges, and Thinking through Different Business Model Types to Maximize Value Capture

There is still much experimentation going on in the industry as to pricing models. Should software be priced in traditional terms (per seat, like traditional SaaS, or usage/token-based like many platform as a service players), or should it be outcomes-based like some companies (Sierra, Salesforce) who are positioning their product as more of a substitute for human labor.

Another debate in the industry involves change management, particularly in fragmented industries or in spaces where AI solutions involve complex integration efforts and leadership buy-in. Some builders have begun to explore whether the value created by an AI transformation could best be captured by owning the service-provider (taking on execution risk for an AI rollout, but benefiting from efficiency gains through AI-driven workflow automation in the form of higher margins) versus simply selling a software solution.

Closing Thoughts

Agentic Solutions have the ability to dwarf the scale of SaaS software, with the ability of technology to now augment and even replace labor and services budgets in an unprecedented way.

AI native companies will be the beneficiaries in this new era, and while there has been tremendous growth and some standout companies that have emerged in certain categories, the space is ripe for builders. Especially in an environment characterized by rapid price decreases in model pricing, and convergence of capabilities, now is an especially exciting time to be building at the application layer.

Subscribed

Share